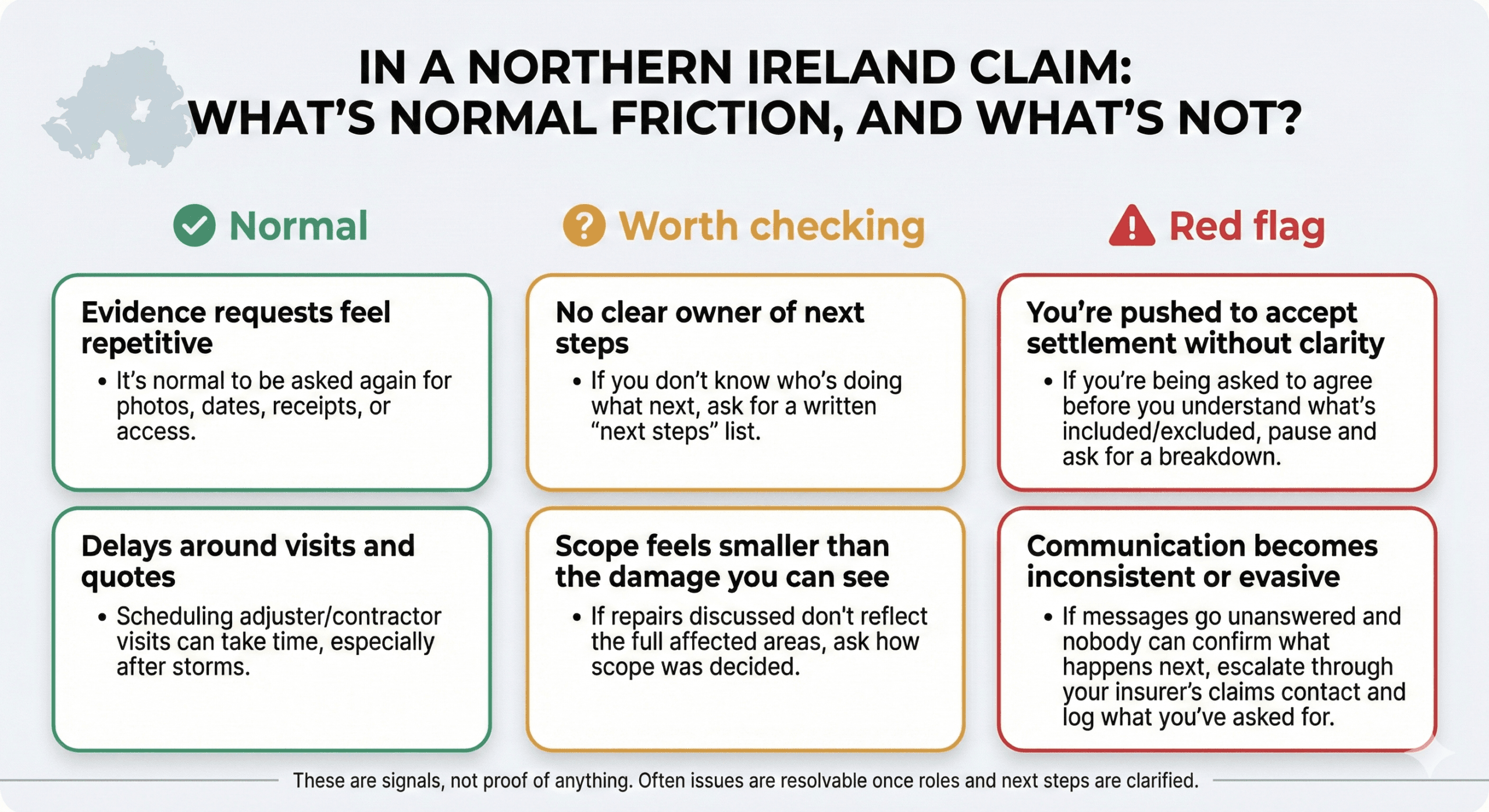

When property damage happens, you will quickly find yourself speaking to people with very similar-sounding job titles. That confusion is common, and it leads to one assumption that costs policyholders money: that everyone involved in your claim is acting in your interest.

This guide explains the difference between a loss assessor, a loss adjuster, and an insurance broker. It covers who each person works for, what they actually do, and when independent representation makes a practical difference to what you receive.

The two questions that cut through the confusion

You do not need to understand the entire UK insurance claims industry to protect your position. You only need to follow two things:

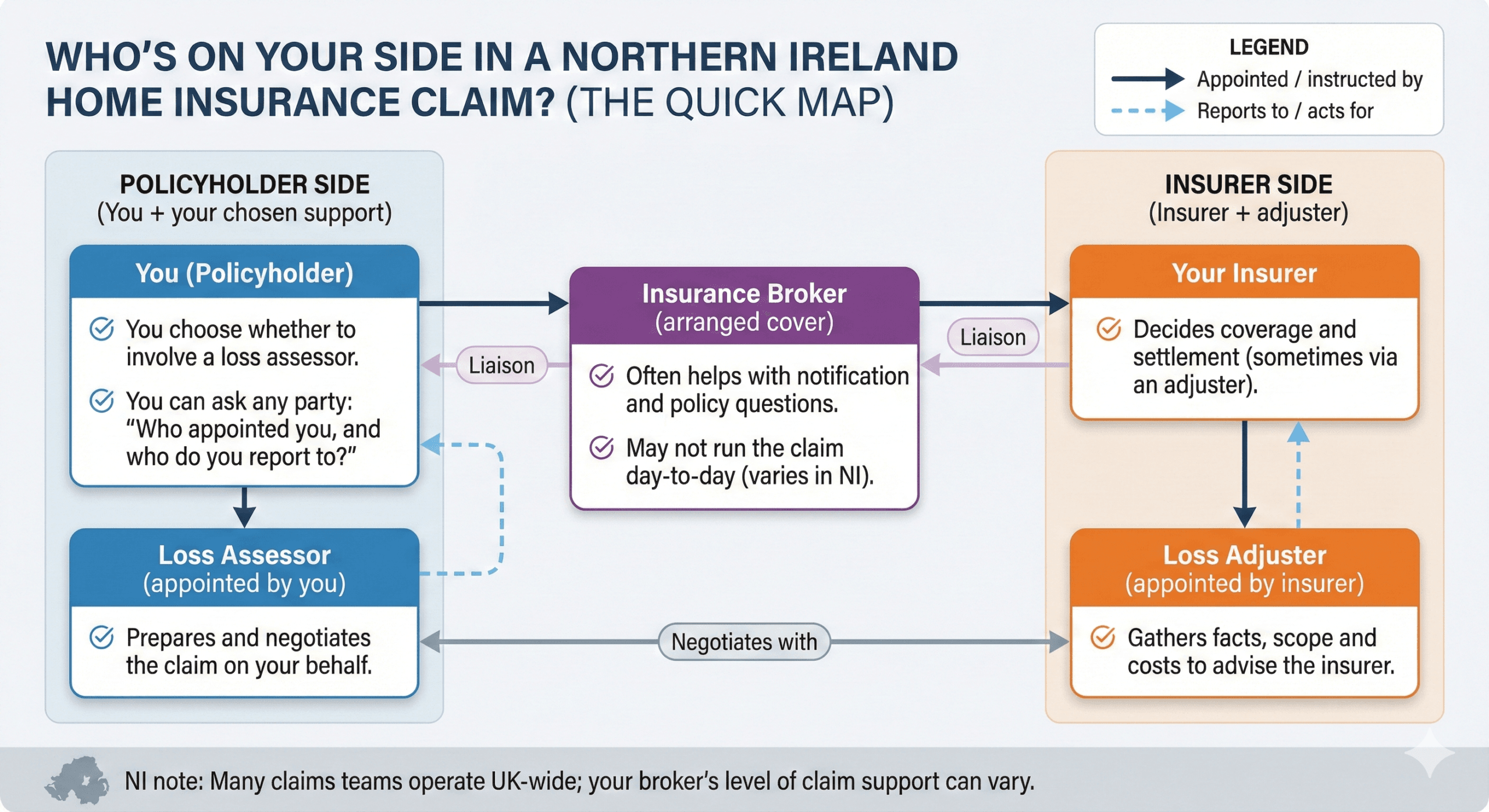

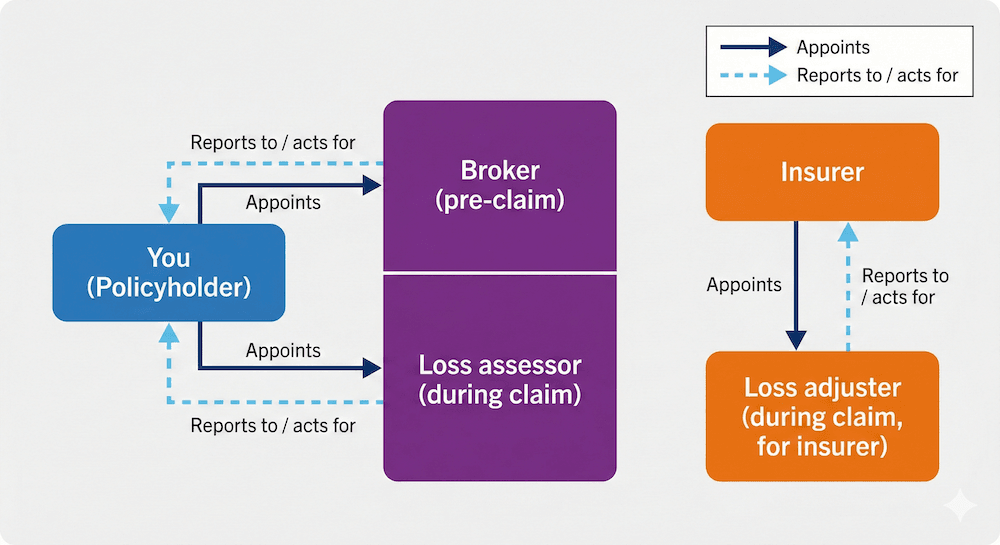

- Who appointed them?

- Who do they report to — and what obligation do they actually owe you?

Apply those two questions to everyone involved in your claim, and the roles become clear.

Who works for whom: the short version

In a property insurance claim in Northern Ireland or Scotland:

- Loss adjuster: appointed by your insurer to assess the claim and report back to them

- Insurance broker: appointed by you to arrange cover, and may offer some support during a claim

- Loss assessor: appointed by you to manage and negotiate the claim on your behalf

The critical distinction is between the loss adjuster and the loss assessor. They sound alike. They are not the same thing.

Quick comparison

| Loss Adjuster | Insurance Broker | Loss Assessor | |

|---|---|---|---|

| Appointed by | Typically the insurer | You, before any claim | You, during a claim |

| Reports to | The insurer | You | You |

| Core role | Investigates, scopes, and recommends settlement to the insurer | Arranges cover; may assist during a claim | Prepares, evidences, and negotiates the claim on your behalf |

| Who they represent | The insurer’s process | You, within the scope of their broking role | You, as your claim representative |

| Fee basis | Paid by the insurer | Fee or commission, paid by you | Paid from settlement — No Win, No Fee |

What does a loss adjuster do — and who do they work for?

When you make a home insurance claim for damage above a few hundred pounds, your insurer will usually appoint a loss adjuster to assess what happened. They will visit your property, inspect the damage, review the policy, and report back to the insurer with their findings.

Loss adjusting — the profession — exists to help insurers manage complex claims accurately and consistently. A loss adjuster’s job is to establish the facts: what caused the damage, what the policy covers, and what a fair settlement figure looks like within the terms of the policy.

They are appointed by the insurer. They are paid by the insurer.

That is not a criticism of loss adjusters as individuals. Most carry out their inspections thoroughly and professionally. But their professional duty runs to the insurer who instructed them, not to you — and that distinction matters when a large sum of money is at stake.

What a loss adjuster assesses

During a survey, a loss adjuster will typically:

- Inspect the visible damage and note its extent

- Identify the probable cause and whether it falls within a covered peril under the policy (storm, fire, escape of water, and so on)

- Look for policy conditions that may limit the claim — pre-existing damage, lack of maintenance, or gradual deterioration

- Estimate the cost of reinstatement using industry pricing tools

- Apply any applicable policy deductions — including excess, underinsurance, or betterment (more on that below)

Their written report becomes the basis of the insurer’s settlement offer. If the offer feels low, the report is usually the place to start.

What a loss adjuster is not

A loss adjuster is not your advocate. They are not there to help you build the strongest version of your claim. That role — assessing the damage on your behalf, evidencing it, and negotiating the settlement with the insurer — is what a loss assessor does.

A loss assessor is appointed by you. They work exclusively for policyholders, never insurers. PCLA operates on a No Win No Fee basis, which means the fee comes from the agreed settlement, not from your pocket upfront.

Loss adjuster tactics — what they mean for your claim

If you’ve searched for “loss adjuster tricks” or “loss adjuster tactics”, you’ve probably received a settlement offer that didn’t match what you expected. You’re not alone. Several tools are available to a loss adjuster that can reduce the amount an insurer pays, and most policyholders don’t know about them until they’ve been applied.

These are not unlawful. They are legitimate professional techniques. But understanding them changes how you respond.

Wear and tear deductions

Most home insurance policies cover sudden, accidental damage — not the gradual deterioration of a property over time. A loss adjuster may inspect damaged roof tiles, pipework, or flooring and conclude that some portion of the damage pre-dates the event being claimed. The settlement offer is then reduced accordingly.

This is often reasonable. But “wear and tear” can be applied broadly. If a pipe failed because it was old, that may be wear and tear — but if it failed because of a sudden freeze, the event itself may be the proximate cause regardless of the pipe’s age. The distinction matters, and it is worth challenging if you believe the deduction is excessive.

Betterment

Betterment is one of the most commonly misunderstood deductions in residential claims. See the FAQs further down the page for more info.

Scope disputes

Loss adjusters estimate reinstatement costs using standard trade rates. In some cases — particularly after water damage, fire, or subsidence — the actual cost of restoring a property to its pre-damage condition may exceed the estimate. This is common when the visible damage extends into areas that weren’t fully accessible during the initial inspection, or when reinstatement involves materials that aren’t straightforwardly interchangeable.

If the scope of the repair is narrower than what you and your contractor believe is necessary, this is a negotiable position, not a final verdict.

The investigation process

For larger claims, or where the cause of damage is unclear, an insurer may ask a loss adjuster to investigate more thoroughly before settling — or may appoint a specialist investigator separately. This can delay the claim significantly.

Being investigated does not mean the claim will be denied. But it does mean the evidence pack you submit matters more. A loss assessor can prepare and manage that evidence so that the investigation process doesn’t turn against you.

What you can do

If a loss adjuster has visited your property and the settlement offer is lower than you expected, you have the right to challenge it. A loss assessor can review the report, identify where deductions have been applied, and negotiate directly with the insurer or loss adjuster on your behalf.

You do not have to accept the first offer.

What a broker does

Your broker’s primary role is before anything goes wrong: arranging suitable cover, explaining policy terms, and ensuring your sums insured are set correctly.

During a claim, many brokers will:

- Help you notify the insurer

- Explain what the insurer is likely to ask for

- Chase progress and keep communication moving

- Clarify policy wording

Most brokers, however, do not have a dedicated claims management function. Where a claim becomes contested, complex, or high in value, a broker is unlikely to prepare a full evidence file, produce a schedule of works, or negotiate directly with the loss adjuster on the technical detail. That is not a criticism — it is simply not what most brokers are set up to do.

A question worth asking your broker early:

“In practice, what do you do during a claim, and what do I need to manage myself?”

A good broker will answer that clearly. Understanding where their involvement ends helps you decide whether you need additional support before the claim is in full swing.

What a loss assessor does

A loss assessor is appointed by the policyholder — you — to manage the claim from your side.

Where the insurer has a loss adjuster preparing their position, a loss assessor prepares yours.

In practice, this means:

- Inspecting the damage and identifying everything that forms part of the claim, including secondary and consequential damage that is easy to overlook

- Preparing a full evidence file: photographs, moisture reports, technical assessments, inventories, contractor evidence

- Producing a detailed scope of works aligned to your policy cover

- Managing all communication with the insurer, the loss adjuster, and appointed contractors

- Challenging scope reductions, low settlement offers, or exclusion decisions that are applied incorrectly

- Negotiating the final settlement figure on your behalf

PCLA’s team includes qualified building surveyors and certified insurance practitioners. For escape-of-water claims, PCLA also provides in-house leak detection using thermal imaging, acoustic equipment, and moisture mapping — producing technical reports that form part of the evidence for the claim.

PCLA operates on a No Win, No Fee basis. If your claim does not succeed, you pay nothing. If it does, the fee is 10% of the final settlement plus VAT. There is no upfront cost and no payment unless the claim results in a settlement.

Practical note on transparency:

UK rules require insurance intermediaries to provide customers with key information about the firm, including how to verify their register status and whether they are representing the customer or acting for the insurer. (Source: FCA Handbook)

Follow the money / follow the duty

Is it too late to appoint a loss assessor?

This is one of the most common questions PCLA receives. The answer is usually: no, it is not too late.

People contact PCLA at every stage: after the loss adjuster has visited, after an initial offer has been made, after a claim has stalled, and after a claim has been rejected outright. In most situations, independent representation is still possible and still useful.

A few points to understand:

- If you have not accepted a settlement offer, there is almost always room to negotiate. An offer is not a final decision.

- If the claim has been disputed or delayed, appointing a loss assessor often accelerates it. The insurer is now dealing with a regulated professional rather than a policyholder managing a complex process on their own.

- If the claim has been rejected, PCLA can review the decision, identify grounds for challenge, and prepare a formal response. A rejection is not necessarily the end.

- If you have accepted a settlement but work has not been completed, contact PCLA, there may still be options depending on the specific circumstances.

The earlier you appoint a loss assessor, the more control they can exercise over how the claim is framed and evidenced. But later is better than not at all.

Will using a loss assessor slow my claim down?

No! In practice, it tends to have the opposite effect.

Delays in insurance claims most commonly occur because documentation is incomplete, the scope of works is disputed, or communication between the policyholder and insurer has broken down. A loss assessor takes over that communication, prepares complete documentation from the outset, and maintains direct contact with the adjuster.

The insurer is now dealing with a regulated claims professional. That tends to sharpen the pace of their decisions.

When does independent representation make a practical difference?

The claim is high value

On a large claim, a difference of even 10–15% in the agreed scope or valuation is a significant sum. That gap frequently exists between the insurer’s initial position and what the policy actually provides.

PCLA secured a settlement of £73,000 on an escape-of-water claim in Belfast due to conducting a full survey, rather than focusing on the visible damage that the homeowner could see. On a water damage claim in Fintona, PCLA secured £11,000 after the policyholder received a disputed offer well below that figure. On a frozen pipe claim in Newry, and a water damage claim in Omagh, similar results followed independent representation.

These are not exceptional cases. They reflect what happens when a claim is prepared properly and the insurer’s initial position is challenged with evidence.

The cause of damage is disputed

This is where loss assessors do their most important work. Two disputes arise repeatedly in Northern Ireland and Scotland:

The “gradual damage” exclusion on oil leak claims (Northern Ireland):

Northern Ireland has a far higher proportion of oil-heated properties than the rest of the UK. Oil leak claims are common — and frequently disputed. The insurer’s standard response is to argue the leak developed gradually over time, making it excluded from sudden damage cover. PCLA prepares the evidence case to challenge that position: independent contamination reports, timeline evidence, and detailed assessments of internal and external damage.

The “wear and tear” reduction on storm damage claims (NI and Scotland):

After a storm, the adjuster will inspect your roof and structural damage. A common outcome is an offer that attributes part of the damage to pre-existing wear rather than the storm itself, reducing both the scope and the settlement. Challenging that requires evidence: weather data, photographs, maintenance records, and where necessary an independent surveyor’s assessment. Without that, the insurer’s position stands.

The damage is hidden or complex

Escape-of-water claims are among the most commonly underpaid claim types in the UK. The initial offer often covers visible damage only. The problem is that water moves — behind plasterwork, under floors, through joists — and the true extent rarely shows on the surface.

PCLA’s in-house leak detection service uses thermal imaging and moisture mapping to document concealed damage and produce a technical report that the insurer cannot easily dismiss. That report forms part of the evidence file for the claim.

You do not have the time or capacity to manage it

A contested claim involves site visits, contractor quotes, detailed policy interpretation, and sustained communication with the insurer and adjuster. Most policyholders are already managing the disruption of a damaged home or property. Managing a complex claim alongside that is a significant demand.

The insurer wants to use their own contractor

You are not obliged to accept the insurer’s managed repair route. If the proposed scope does not fully reinstate your property, or you have concerns about the insurer’s appointed contractor, a loss assessor can intervene before work begins to ensure the scope is correct and your interests are protected.

Do you always need a loss assessor?

No. For a straightforward, low-value, clearly evidenced claim where the insurer is progressing quickly and the offer reflects the actual damage, managing it yourself is entirely reasonable.

A loss assessor is most useful when the claim is high in value, complex in scope, disputed in cause, or demanding in terms of time and management. Because PCLA operates on a No Win, No Fee basis, you can request a free review of your claim with no commitment and decide from there whether independent support is the right step.

If you want to work through the decision in more detail, the guide Do I need a loss assessor? sets out the factors clearly.

How PCLA works alongside your broker

There is no conflict between using a broker and appointing a loss assessor. In practice, the two roles sit alongside each other.

Many of PCLA’s instructions come through broker referrals. Where a broker recognises that a claim has become too complex or too contentious for their client to manage alone, they refer to PCLA to handle the claim management. The broker remains the client’s insurance relationship. PCLA manages the evidence, the scope, the negotiation, and the day-to-day claim process.

Questions people ask when they’re trying to work out “who is on my side”

What is loss adjusting?

Loss adjusting is the professional practice of investigating and evaluating insurance claims on behalf of an insurer. A loss adjuster inspects the damaged property, determines the cause and extent of the loss, checks what the policy covers, and produces a report that the insurer uses to settle the claim.

What does a loss adjuster do?

A loss adjuster visits the property, assesses the damage, reviews the insurance policy, and provides the insurer with a written report recommending a settlement figure. They may also manage the repair process in some cases. Their professional duty is to the insurer, not the policyholder.

What is the difference between a loss assessor and a loss adjuster?

A loss assessor works for the policyholder. A loss adjuster works for the insurer. Both are claims professionals, but they are on different sides of the negotiation. See the full comparison at the top of this page.

Can I challenge the loss adjuster’s valuation?

Yes. A loss adjuster’s settlement recommendation is not final. You can dispute the amount — either directly with the insurer, or through a loss assessor who can review the report, challenge specific deductions, and negotiate a revised figure. If the claim cannot be resolved, it may be referred to the Financial Ombudsman Service.

What is betterment in insurance?

Betterment is a deduction applied when an insurance repair results in an improvement to the property beyond its pre-damage condition. The principle: insurance is intended to restore what you had, not to leave you better off.

Example: A burst pipe damages a section of flooring that was installed 15 years ago. If the insurer replaces it with new flooring of equivalent specification, the policyholder arguably ends up with something worth more than what they lost. The insurer may apply a betterment deduction — typically a percentage reduction based on the age of the damaged material — to reflect that difference.

Betterment deductions are most common in:

- Flooring (carpets, hardwood, tiles)

- Kitchen and bathroom fittings

- Roofing materials

- Paintwork and decorating

When betterment can be challenged

Betterment is a legitimate deduction, but it can be applied inconsistently or at an excessive rate. Factors that may support a challenge include:

- The original material is still in production and can be replaced like-for-like (betterment may not apply)

- The deduction percentage is higher than the actual age and condition of the material warrants

- The claim involves a structural element where matching materials are a regulatory or practical requirement

- The insurer is applying betterment to labour costs as well as materials (unusual and generally unjustified)

A loss assessor can review how betterment has been applied to your settlement and, where the deduction is excessive, negotiate a reduced figure.

What does “assessor in insurance” mean?

In a home insurance claim context, an assessor — or loss assessor — is an independent professional appointed by the policyholder to manage the claim on their behalf. They assess the damage, prepare the evidence, and negotiate the settlement with the insurer. They are distinct from a loss adjuster, who is appointed by and works for the insurer.

What is loss adjuster meaning in UK insurance?

A loss adjuster is an insurance professional appointed by an insurer to investigate a claim and recommend a settlement. “Loss adjusting” refers to the process of adjusting (settling) a loss within the terms of the policy. In UK residential claims, a loss adjuster visit typically follows a claim for significant property damage — fire, flood, escape of water, storm, or similar.

Who does the loss adjuster work for?

The loss adjuster is appointed and paid by your insurer. Their role is to investigate the claim, scope the damage, and recommend a settlement position to the insurer. They are not your representative. They can conduct a thorough inspection and still report findings that serve the insurer’s interest rather than yours.

Is it too late to appoint a loss assessor if the loss adjuster has already visited?

No. You can appoint a loss assessor at any point during a live claim — after the adjuster has visited, after an offer has been made, and in most cases after a claim has been disputed or rejected. Contact PCLA for a free review of where your claim stands before you accept any decision as final.

Will a loss assessor slow my claim down?

No. In practice, it tends to accelerate it. Delays occur when documentation is incomplete or communication breaks down. A loss assessor takes over both, which typically sharpens the pace of the insurer’s decision-making.

What does PCLA charge?

PCLA operates on a No Win, No Fee basis. There is no upfront cost. If the claim does not succeed, there is no charge. If it does, the fee is 10% of the final settlement plus VAT.

Should I contact PCLA before or after I notify my insurer?

Before, if possible. That way, PCLA manages the notification, frames the claim correctly from the start, and ensures nothing is admitted or agreed that limits your position later. If you have already notified the insurer, PCLA can take over the management of the claim from that point.

My insurer says the damage is wear and tear — what can I do?

Wear and tear is a legitimate exclusion, but it is regularly applied too broadly. The insurer must demonstrate that the damage was caused by gradual deterioration rather than an insured event. If you have evidence of the event and the timing of the damage, that position can often be challenged. PCLA handles these disputes regularly across both Northern Ireland and Scotland.

Can a loss assessor help if my claim has been rejected?

Yes. A rejection is not necessarily final. PCLA can review the decision, identify whether it was applied correctly under the policy wording, prepare a formal challenge, and if necessary refer the matter to the Financial Ombudsman Service. Do not accept a rejection without getting an independent view first.

Does PCLA cover Scotland as well as Northern Ireland?

Yes. PCLA operates across all of Northern Ireland and across Scotland, principally in the Central Belt from Glasgow to Edinburgh. Both regions have distinct claim patterns, local insurer processes, and common dispute types — PCLA’s team has direct experience in both.

The insurer wants to use their own contractor — do I have to agree?

No. You are entitled to obtain independent repair quotations. If the insurer’s managed repair route does not reflect the full reinstatement scope, you can challenge it. PCLA can intervene before any work begins to ensure the scope is accurate and that you are not committed to a repair process that does not properly restore your property.

What types of claim does PCLA handle?

Water damage, escape of water, fire and smoke damage, storm and roof damage, flood damage, oil leaks and contamination, impact damage, theft and malicious damage, landlord claims, commercial property claims, and business interruption. PCLA also provides in-house leak detection to support escape-of-water claims that require technical evidence.

If the settlement feels wrong, speak to PCLA first

A low settlement offer doesn’t have to be the end of the conversation. If a loss adjuster has surveyed your property and the figure doesn’t reflect the damage you’ve seen, there may be grounds to challenge the assessment — whether that’s a wear and tear deduction you weren’t expecting, a betterment reduction that’s been applied too aggressively, or a scope of works that doesn’t cover everything that needs repairing.

PCLA acts exclusively for policyholders. We don’t work for insurers, loss adjusters, or contractors. Our role is to assess the damage independently, build the evidence, and negotiate the settlement on your behalf.

No Win No Fee.

If you’re in Northern Ireland or Scotland and a claim isn’t going the way you expected, call us before you respond to the insurer’s offer.

Northern Ireland: 028 9581 5318

Scotland: 0141 461 2406

Related guides: